As the planet continues to grapple with the response to the COVID-19 pandemic, full recovery at a global scale is still not in sight, nor is it guaranteed. Variations and mutations continue to emerge, leading to hotspots and ‘breakthrough’ infections of those already vaccinated. The emergence of this once-in-a-century global pandemic highlights how we continue to be susceptible to massive external shocks and ‘black swan’ events. What is clear is that the role of digital technologies and digital infrastructure is as important as ever in building resilience and response capabilities as discussed below and in Chapter 2. And while the future is yet to be written, we can identify major trends related to broadband and digital infrastructure that the pandemic has either highlighted or heightened, particularly in the case of major drivers of change.

The centrality of connectivity has been crystalized in public life

The shutdowns around the world in 2020, with some continuing in 2021, highlighted the need for robust communications infrastructure, particularly broadband, to continue economic and social activities. The International Labour Organization (ILO) estimates that in 2020 the world lost 8.8 per cent of global working hours (compared to previous years), with an equivalence of 255 million full-time jobs (based on a 48-hour work week). This figure represents nearly four times the losses incurred during the global financial crisis of 2008.

The ability for workers to continue employment during the pandemic differed significantly on the basis of the nature of the employment (for example between informal in-person, manufacturing, services or knowledge activities, among others) and the robustness of the communications infrastructure workers have access to. In the United States, nearly half of the US labour force moved to working remotely from home during the peak of the crisis, up from 15 per cent previously. Across a range of countries, the share of previously employed individuals who were able to continue working remotely from home or had to stop working completely differed widely. And more generally, 83 per cent of smartphone users claim that ICT helped them a great deal in coping during COVID-19 imposed lockdowns. In many countries, constraints to basic access to Internet or ownership of computers exert a gating constraint to remote work opportunities in times of crisis.

While much economic, learning and even healthcare activity was able to shift online, the pandemic highlighted the importance of effective and robust digital infrastructure.

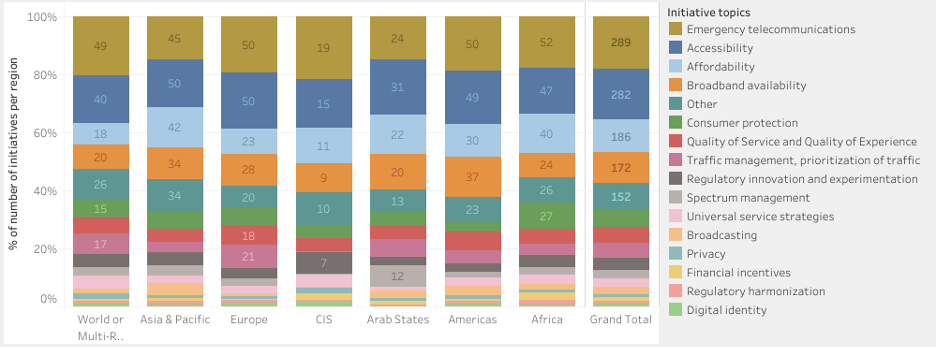

This realization has led to significant immediate and long-term policy responses by governments, and investments by commercial and other entities. Chapter 2 provides much detail on the range of policy responses, including some of the 480+ ICT policy actions tracked in the REG4COVID ITU tracker alone, across various dimensions including emergency telecommunications, accessibility, affordability, broadband availability, etc.

ICT Policy Responses to COVID-19, worldwide and by region (ITU REG4COVID)

While many of these measures were temporary, the impact of COVID-19 on the nature of remote-based engagements (be it economic activity, learning, medical, or entertainment-focused, among other activities) may become much more permanent as more individuals transition more of their activities online and new users join the digital economy. Historically, the adoption and utilization of the Internet by new users, as well as existing users who upgrade to higher speed connections, demonstrate a virtuous circle of ever-increasing extensive and intensive data use (more users, and more data per user). Since 2000, Internet users have increased ten-fold from around 400 million users to more than 4 billion users today. More intensive data uses are leading to different behaviours and eventually life outcomes. For example, Ericsson’s recent ConsumerLab report, the largest consumer report of its kind, shows that 5G users spend two hours more per week on cloud gaming, one hour more on AR apps and one hour more consuming live broadcasts compared to 4G LTE users. Globally, total data consumption has increased 283-fold from 0.2 exabytes per month in 2011, to 166 exabytes in 2021.

A lingering digital divide remains, exacerbated by the pandemic

While overall and individual data consumption increased during the pandemic, it remains to be seen what the net effect on total users will be; while the crisis has brought many new users online, others have had to limit or stop their access because of the economic impact to income and affordability that most affects populations that use the Internet the least. As the world shifted to online engagement in the second quarter of 2020, Internet traffic growth significantly outpaced pre-COVID-19 era forecasts: average traffic in 2020 grew by 48 per cent while global peak traffic grew by 47 per cent, compared to forecasts of average annual growth between 2016 and 2020 of 30 per cent. Globally, last year consumers’ use of fixed broadband increased by an average of two and a half hours per day, and on mobile by one hour. Similarly, 60 per cent of white-collar workers increased their use of video calls. In the US and Europe in particular, traffic on broadband networks increased 51 per cent because of the COVID-19 pandemic, and average per-subscriber (or household) usage increased from 344 GB per subscriber in Q4 of 2019 to 482.6 GB per month in Q4 of 2020, an increase of 40 per cent.

The digital divide exacerbates the negative social impacts of the COVID-19 pandemic and threatens to exacerbate overall divides. For example, learners at all ages and levels were, and in many countries still continue to be, significantly affected by the pandemic in part due to a lack of remote learning ability. School closures occurred across 190 countries, impacting more than 91 per cent of students worldwide at an estimate of 1.6 billion children and young people. At least 31 per cent of schoolchildren worldwide (463 million) cannot access distance education content via Internet access or broadcast technologies for a range of reasons including a lack of necessary technologies, among others.

And the nature of COVID-19 itself, leading to contagion based on direct exposure and physical proximity to infected individuals, further stresses the need to be able to treat patients of all kinds (with COVID-19 and with other ailments) safely at a distance through telemedicine options. But even today, limited broadband adoption not only hampers future development and resilience, it is also impacting COVID-19 response activities. For example, in India, where a significant resurgence of COVID-19 swept across the country in April and May 2021, the government imposed a requirement that by May 1, citizens between the age of 18 and 45 had to register in advance for vaccination online and could not walk-in for vaccination. However, nearly 50 per cent of the population does not have access to the Internet.

Even within developed countries, the pandemic has exposed digital divides between populations, communities and ethnic groups, and has been a wake-up call that efforts to simply apply more infrastructure and more technology at cheaper prices do not fully address systemic differences between peoples. More targeted interventions that are cognizant of social inequalities, and the complexities of digital disparities are required.

Shifting from network expansion to network densification

Global networks (terrestrial, space and undersea) across various technologies and dimensions combine to reach and cover every part of the world; the challenge now is ensuring sufficient capacity, competition, and affordability while continuing to attract sustainable investments into networks, services, technologies and capacities. According to mobile network carriers, only 7 per cent of the world’s total population reside in geographic areas where they cannot provide mobile Internet connectivity (at least 3G data service). These 570 million people outside of at least 3G cellular coverage may still have some connectivity via 2G for voice and basic text message functionality, though 2G and 3G services are now starting to be shut down in order to re-farm spectrum for 5G, and in some cases for 4G in emerging markets. These transitions will have to be managed carefully as significant numbers of mobile users around the world, in developing as well as developed countries, continue to use 2G and 3G devices for a wide range of reasons, including affordability, limited digital skills and familiarity, as well as limits to service options. Shutdowns will force many of these users to transition and many may not be ready to do so. For example, in the United States, estimates range between 13 to 17 per cent of mobile subscribers still relying on 2G and 3G services, which amounts to a significant share of the subscriber base. Technology neutral spectrum regulations are key to enable mobile operators to smoothly transition users to new generation networks, increasing network capacity but avoiding shutting down old networks that may affect those who cannot afford new devices.

While 85 per cent of the world’s population are already covered by 4G networks, nearly half of them are still offline, in part because of the relatively high price of Internet access (though some geographies and populations remain economically unviable and governments and industry players continue to work together to find ways to ensure digital inclusion). Building broadband connectivity on top of existing mobile broadband infrastructure is a fast and cost-efficient option to bridge the digital divide.

It is also important to note in the overall context and trend of network expansion and network densification that in many cases, these various technologies (wireless, wired, and satellite) are more complementary rather than in direct competition, as connectivity has become so pervasive to daily life there is a plethora of needs, demands, constraints, and use cases for which each technology and service may be best fit (for example indoor versus outdoor, local area versus wide area, and in last mile versus backhaul). And though 5G is still in early stages of deployment, work is already being done on setting the policy and technical foundations for 6G with the launch of the Next G Alliance and the European Commission’s 6G research initiative, project Hexa-X.